Sea Limited

Background

The bull case narrative for SE is known -- SE will win the food fight and dominate the South East Asia eCommerce industry. However, while the narrative is out there, it is unclear how that ties to the ultimate financials and valuation. Is this company still attractive at a $25bn valuation? $40bn valuation?

The bull case narrative for SE is known -- SE will win the food fight and dominate the South East Asia eCommerce industry. However, while the narrative is out there, it is unclear how that ties to the ultimate financials and valuation. Is this company still attractive at a $25bn valuation? $40bn valuation?

In order to better understand the risk reward, we need to tie the narrative to the financials. This blog post is focus on this. My approach uses a combination of analog and market size estimate to triangulate the company's future earnings profile.

Framing Shopee’s upside

Formula:

E-commerce TAM × Shopee Market Share → GMV

× Shopee Take Rate → Shopee Revenue × NTM EV/Revenue Multiple → Shopee’s Value

I believe that the TAM will be about $122bn in 2025. This was estimated through a combination of third-party sources (LINK) and analog in other regions.

Note: Taiwan est. TAM ~20bn in 2025

Of the $122bn market size, my base rate is that SE will maintain its 33% market position that it has today, with the rest of the market split between the other eCommerce players and retail brands own eCommerce channel.

Lastly, I believe SE will be able to bring its take rate up from 3.6% today to 8% in the future, closer to peers such as MELI and AMZN.

Solving for 2025 revenue

Multiplying all of this together suggests a $3.2bn revenue potential

$122bn × ~33% × 8% = $3.2bn revenue

Shopee valuation

I believe that MELI will be the closest comp to SE in terms of size and growth by 2025, and as such would serve as a good analog to what SE might we worth today. In the bull case, I attach MELI existing 10x revenue multiple to SE's eCommerce business in 2025, and discounted it back to present value.

Doing suggests a market value of nearly $20bn, or ~$44/share

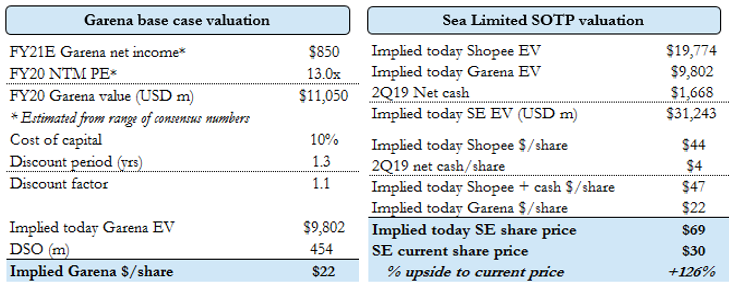

SE valuation

To round things up, lets add the value of Garena and SE's cash into our calculation to get to SE's value if everything goes right. Based on these assumptions, SE can be worth >2x its current

share price with large part of value accruing to Shopee (~64% of value).

Am I bullish on SE? Yes. At the current valuation, the

risk reward is appealing.

Shopee has executed fabulously on its growth

strategies so far, evident by the numbers. Can Shopee continue executing? I

love to think it can, but I guess we will only know as things play out.

Comments

Post a Comment