Deliveroo $7bn valuation...Really?

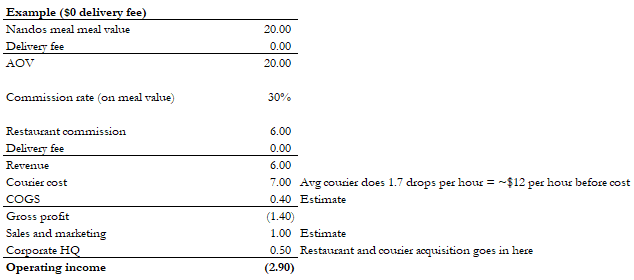

Please find updated post here: https://newmooncap.substack.com/p/deliveroo-7bn-valuationreally What about Deliveroo? $7bn valuation! And it is profitable! I find this valuation pretty absurd, although I am pretty sure whoever made this investment in Durable would still make money in the IPO pop. I have a few concerns: Notice that Deliveroo only said it is profitable on an operating level. What does this mean? Does this exclude corporate HQ costs such as restaurant and courier acquisition? How profitable would Deliveroo be post-Covid? I am guessing Covid benefited the company’s unit economics by increasing AOV, willingness to pay a delivery fee, and reducing CAC (S&M). MOST IMPORTANTLY , we know that Deliveroo is only profitable because the company do two things: (1) charge a high delivery fee, (2) lower courier fee per hour, and (3) shrink courier radius to ensure higher drop velocity and therefore further lowering delivery fee per drop This should allow Deliveroo to be pr...